If you own a profitable, unincorporated business with your spouse, you're probably fed up with high self-employment (SE) tax bills.

If you own a profitable, unincorporated business with your spouse, you're probably fed up with high self-employment (SE) tax bills.

An unincorporated business in which both spouses are active is typically treated as a partnership that's owned 50/50 by the spouses — or a limited liability company (LLC) that's treated as a partnership for tax purposes and owned 50/50 by the spouses. In either case, you and your spouse must separately calculate your respective SE tax bills.

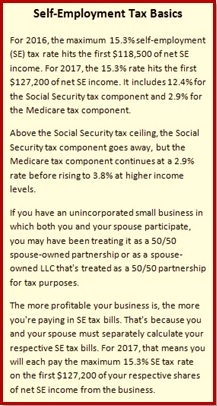

For 2017, that means you'll each pay the maximum 15.3% SE tax rate on the first $127,200 of your respective shares of net SE income from the business. (See "Self-Employment Tax Basics" below.) Those bills can mount up if your business is profitable. Here are three ways spouse-owned businesses can lower their combined SE tax hit.

-

Establish that You Don't Have a Spouse-Owned Partnership (or LLC)

Establish that You Don't Have a Spouse-Owned Partnership (or LLC)

To illustrate the adverse tax consequences of operating a spouse-owned partnership, suppose you expect your business to generate $250,000 of net SE income in 2017. You and your spouse must separately calculate SE tax. So each of you will owe $19,125 ($125,000 x 15.3%), for a combined total of $38,250. To make matters worse, your SE tax bill is likely to increase every year due to inflation adjustments to the Social Security tax ceiling and the growth of your business.

These adverse effects apply only if you have a business that is properly treated as a 50/50 spouse-owned partnership or a spouse-owned LLC that's properly treated as a 50/50 partnership for federal tax purposes.

Several IRS publications attempt to create the impression that involvement by both spouses in an unincorporated business automatically creates a partnership for federal tax purposes. For example, the Tax Guide for Small Business says, "If you and your spouse jointly own and operate an unincorporated business and share in the profits and losses, you are partners in a partnership, whether or not you have a formal partnership agreement."

However, in many cases, the IRS will have a tough time making the argument that a business is a 50/50 spouse-owned partnership (or LLC). Consider the following quote from an IRS private letter ruling: "Whether parties have formed a joint venture is a question of fact to be determined by reference to the same principles that govern the question of whether persons have formed a partnership which is to be accorded recognition for tax purposes. Therefore, while all circumstances are to be considered, the essential question is whether the parties intended to, and did, in fact, join together for the present conduct of an undertaking or enterprise."

The IRS private letter ruling identifies these factors, none of which is conclusive, as evidence of this intent:

- The agreement of the parties and their conduct in executing its terms,

- The contributions, if any, that each party makes to the venture,

- Control over the income and capital of the venture and the right to make withdrawals,

- Whether the parties are co-proprietors who share in net profits and who have an obligation to share losses, and

- Whether the business was conducted in the joint names of the parties and was represented to be a partnership.

In many situations where both spouses have some involvement in an activity that has been treated as a sole proprietorship or in an activity that has been operated as a single-member LLC (SMLLC) that has been treated as a sole proprietorship for tax purposes, only some of the factors listed in the private letter ruling are present. Therefore, the IRS may not necessarily succeed in arguing that the business is a spouse-owned partnership (or LLC).

That argument may be especially weak when:

- The spouses have no discernible partnership agreement, and

- The business hasn't been represented as a partnership to third parties, such as banks and customers.

If your business can more properly be characterized as a sole proprietorship or as an SMLLC that is treated as a sole proprietorship for tax purposes, only the spouse who is considered the proprietor owes SE tax.

Let's assume the same facts as in the previous example, except that you take a supportable position that your business is a sole proprietorship operated by one spouse. Now you have to calculate SE tax for only that spouse. For 2017, the SE tax bill would be $23,023 [($127,200 x 15.3%) + ($122,800 x 2.9%)]. That's much less than the combined SE tax bill from the first example ($38,250).

-

Establish That You Don't Have a 50/50 Spouse-Owned Partnership (or LLC)

Establish That You Don't Have a 50/50 Spouse-Owned Partnership (or LLC)

Not all businesses are owned 50/50 by their owners. Say your business can more properly be characterized as a partnership (or LLC) that's owned 80% by one spouse and 20% by the other spouse, because one spouse does much more work than the other.

This time, let's assume the same facts as in the previous example, except that you take a supportable position that your business is an 80/20 spouse-owned partnership (or LLC). In this scenario, the 80% spouse has net SE income of $200,000, and the 20% spouse has net SE income of $50,000.

For 2017, the SE tax bill for the 80% spouse would be $21,573 [($127,200 x 15.3%) + ($72,800 x 2.9%)], and the SE tax bill for the 20% spouse would be $7,650 ($50,000 x 15.3%). The combined total SE tax bill is $29,223 ($21,573 + $7,650), which is significantly lower than the total from the first example ($38,250).

READ MORE: How Businesses Can Save Federal Employment Taxes: Become an S Corporation

- Liquidate Spouse-Owned Partnership and Hire One Spouse as an Employee

This strategy is a little more complicated than the previous strategies. First, you'll need to dissolve your existing spouse-owned partnership or spouse-owned LLC that's treated as a partnership for federal tax purposes, and start running the operation as a sole proprietorship or SMLLC treated as a sole proprietorship for federal tax purposes. Even if the partnership (or LLC) owns assets and has liabilities, this step is generally a tax-free liquidation under the partnership tax rules.

The second step is to hire one spouse as an employee of the new proprietorship (SMLLC). Pay that spouse a modest cash salary, and withhold 7.65% from the salary checks to cover the employee-spouse's share of Social Security and Medicare taxes. As the employer, the proprietorship must pay another 7.65% directly to the government to cover the employer's half of Social Security and Medicare taxes. However, since the employee-spouse's salary is modest, the Social Security and Medicare tax hits will also be modest.

The third step is to consider setting up a Section 105 medical expense reimbursement plan for the employee-spouse. Use the plan to cover your family's out-of-pocket medical expenses, including health insurance premiums, by making reimbursement payments to the employee-spouse out of the proprietorship's business checking account. Deduct the plan reimbursements as a business expense of the proprietorship. On the employee-spouse's side of the deal, the plan reimbursements are free of federal income, Social Security and Medicare taxes because the plan is considered a tax-free fringe benefit.

The fourth step is to deduct, on the sole proprietorship's (SMLLC's) tax schedule, the medical expense plan reimbursements, the employee-spouse's cash salary, and the employer's share of Social Security and Medicare taxes. These deductions also reduce the proprietor's net SE income and the SE tax bill for the business.

Finally, you'll need to calculate the SE tax bill for the spouse who is treated as the proprietor. This minimizes the SE tax hit, because the maximum 15.3% SE tax rate applies to no more than $127,200 of SE income (for 2017), vs. up to $254,400 if you continue to treat your business as a 50/50 spouse-owned partnership (or LLC).

Important note: If you have employees other than the spouse, your business may have to cover them under a Section 105 medical expense reimbursement plan.

Contact Us

SE taxes can quickly add up, but there are several strategies that spouse-owned businesses can use to reduce their combined total bill. Contact us before using any of these strategies to avoid any potential pitfalls and make the optimal choice for your business.

© 2017