The Section 179 deduction for qualified real property expenses was made permanent under the Protecting Americans from Tax Hikes (PATH) Act of 2015. However, claiming this deduction isn't a no-brainer. Here are the pros and cons.

The Section 179 deduction for qualified real property expenses was made permanent under the Protecting Americans from Tax Hikes (PATH) Act of 2015. However, claiming this deduction isn't a no-brainer. Here are the pros and cons.

Deductions for Qualified Real Property Costs

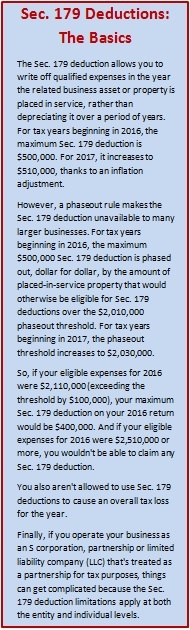

Not too long ago, real property costs weren't eligible for the Sec. 179 deduction, and then they were made eligible but subject to lower deduction limits than other assets eligible for the deduction. (See "Section 179 Deductions: The Basics" below.) Now deductions claimed for real property are included in the overall Sec. 179 deduction maximum of $500,000 for 2016 and $510,000 for 2017.

Qualified real property costs include the following:

Qualified real property costs include the following:

- Qualified improvement property costs: These include interior building costs for nonresidential buildings. Certain interior costs are excluded, such as the cost of elevators and any interior structural framework of the building. The improvements must be placed in service more than three years after the date the building was first placed in service. For the 2016 deduction, the property in question must have been leased.

- Qualified restaurant property costs: These include both building and improvement costs. To qualify as restaurant property, more than 50% of the building's square footage must be devoted to the preparation of meals and seating for on-premises consumption of meals.

- Qualified retail improvement costs: These include nonresidential building interior costs for a building that's open to the general public and used to sell tangible personal property. Certain interior costs are excluded, such as the cost of elevators and any interior structural framework of the building. The improvements must be placed in service more than three years after the date the building was first placed in service.

Immediate Write-Off vs. Regular Depreciation

Claiming a Sec. 179 deduction for a qualified real property expense allows the cost to be completely written off in the first year. In contrast, following the "regular" IRS depreciation rules would generally require the cost to be written off, straight-line, over 39 years. So, there's a significant timing advantage to claiming Sec. 179 deductions.

But there's also a potential downside for real estate gains recognized by individuals: Gains attributable to Sec. 179 deductions will count as ordinary income when the real property is eventually sold.

Ordinary gains recognized by individual taxpayers are taxed at higher rates than long-term capital gains. Under the current rules, the maximum federal income tax rate on an individual's ordinary income is 39.6%. In addition, the 3.8% net investment income tax (NIIT) may apply.

READ MORE: 10 Tax Changes That Could Affect Your 2016 Return

Under tax reform proposals, the maximum rate on an individual's ordinary income would fall to 33%, and the 3.8% NIIT might be abolished as part of the repeal of the Affordable Care Act. As of this writing, however, we don't know when or if these proposals will become law.

On the other hand, if your business claims "regular" depreciation deductions for real estate expenses, long-term gains recognized by individual taxpayers that are attributable to those depreciation deductions are taxed at a maximum capital gains rate of 25% under the current rules. The 3.8% NIIT may also apply.

There is much uncertainty about the tax changes that might become law under the Trump administration and Republican-controlled Congress, as well as the timing of those changes. However, it's likely that ordinary real estate gains attributable to Sec. 179 deductions that are recognized by individuals will continue to be taxed at higher rates than long-term real estate gains that are attributable to regular depreciation deductions.

There is much uncertainty about the tax changes that might become law under the Trump administration and Republican-controlled Congress, as well as the timing of those changes. However, it's likely that ordinary real estate gains attributable to Sec. 179 deductions that are recognized by individuals will continue to be taxed at higher rates than long-term real estate gains that are attributable to regular depreciation deductions.

If so, claiming Sec. 179 deductions for real estate expenses will continue to have a downside when the related property is sold. So, you'll need to weigh that potential downside against the benefit of getting first year write-offs under the Sec. 179 deduction.

Key Point: Under the current rules, long-term real estate gains recognized by individuals that aren't attributable to Sec. 179 deductions or regular depreciation are generally taxed at either 15% or 20%. Under tax reform proposals, those rates are expected to continue.

C Corporation Real Estate Gains

Under the current IRS rules, real estate gains recognized by C corporations are taxed at the same rates regardless of whether they're considered capital gains or ordinary income. So, there's currently no downside to a C corporation claiming Sec. 179 deductions for real estate. It's uncertain whether this will continue to be true under any tax reform legislation that may be signed into law.

Bottom Line

Before taking Sec. 179 deductions for qualified real property expenses, it's important to understand what expenses qualify and what limitations may apply, along with any potential downsides. We’re atop the latest rules and can help you make the most of depreciation-related deductions on your 2016 tax return and in later years. Contact us for personal assistance.

© 2017