Did you feel like your taxes were minimized last year? If not, it’s possible you may have missed out on some opportunities.

Did you feel like your taxes were minimized last year? If not, it’s possible you may have missed out on some opportunities.

Federal tax reform through the Tax Cuts and Jobs Act provided some of the best tax benefits to businesses in more than 50 years. The corporate tax rate was slashed from the graduated maximum of 35% to a flat 21%.

There also was big news for smaller businesses – the new Qualified Business Income Deduction offers possibly the greatest tax benefit to pass-through businesses in more than 60 years. QBI allows qualified small business owners to simply not pay income taxes on 20% of their qualified income in tax years 2018 through 2025.

While every tax situation is different and savings are not guaranteed, most of the businesses we work with had a good 2018 tax year.

Did you? If not, download our free Top 6 Tax Reform Opportunities for Business guide. Learn about the latest tax strategies for businesses to see if you could benefit.

Did you? If not, download our free Top 6 Tax Reform Opportunities for Business guide. Learn about the latest tax strategies for businesses to see if you could benefit.

Download the guide now, or check out one of the six strategies below:

Switching to a C Corporation

While switching to a flat 21% federal tax rate sounds very tempting, there are some downsides with operating as a C Corporation. Here are some of them:

Double taxation: Owners of the corporation pay a double tax on earnings, first at the entity level and then again when profits are distributed out in the form of dividends to shareholders. Dividends are usually taxed at the qualified dividend rate of 20%, though there is usually no preferential tax rate at the state and local level. These dividends may also be subject to the 3.8% net investment income tax, an important (and costly) detail that it often overlooked.

No personal income off-set: Another tax-related downside is that since the C Corporation pays taxes at the entity level and passes no income through to shareholders, those owners are not able to use C Corporation losses in any given year to offset personal income from other sources.

Even more taxes: If the C corp accumulates cash, it can be subject to one of two penalty tax regimes: the accumulated earnings tax and personal holding company tax.

A C corporation is subject to the accumulated earnings tax if it accumulates earnings beyond the reasonable needs of the business. A gray area to be sure, but one to pay close attention to as any extra taxes are bad taxes.

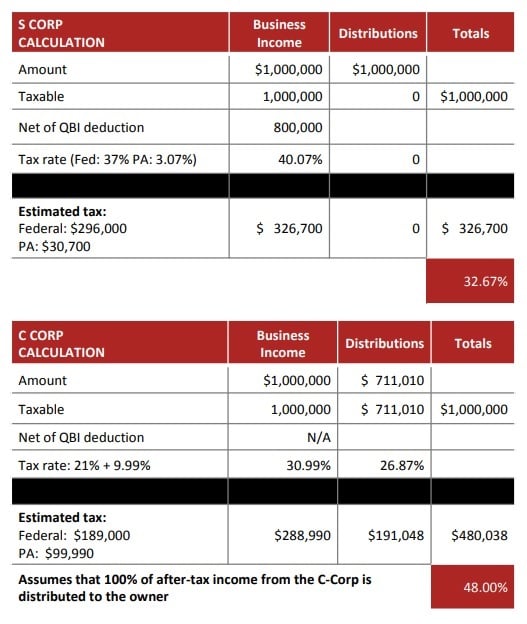

Check out this example using a Pennsylvania-based company with business income of $1 million. As an S Corp, the company would pay $326,700 in federal and state taxes. As a C Corp, the company would pay $480,038 in federal and state taxes. Remaining an S Corp saves $153,338 in taxes.

Want to learn more? Click here to download our complete Top 6 Tax Reform Opportunities for Businesses guide or contact us here.